T W Dyott the Banker

Dyott knew the more control he had on his own supplies and raw materials the larger the profit. Dyott leased the Glass Factory and surrounding property in 1817. He named the village near his factory complex Dyotville. In 1833 he purchased the factory out right and invested tens of thousands of dollars in expanding the size and the number of pots and employees and its adjacent housing. Dyott always managed to acquire needed capital from wealthy local merchants.

Two of these merchants were Jacob Ridgway and Captain Daniel Man. They were the primary source for these funds. Ridgway was one of the most prominent of Philadelphia’s international merchants and had made his considerable fortune as a partner in several large and influential trading companies. He was Dyotts most dependable source of needed funds over several decades. He made his money from Dyott by giving the Doctor a heavy discount rate on his promissory notes. Captain Man was an even more aggressive financier. “I played the game of the lawyers when they get hold of a fat client, make as much as they can,” the Captain stated in describing his lending relationship with Dyott. “I got always as much from the Doctor as I could from any body else. I shaved everyone as close as I could and Dyott was no exception.”

Dyott estimated that he paid about $50,000 in “shaving interest” on his Dyottville factory alone over a twenty year period and on his various businesses generally “paid usury to the amount of $15,000 to 30,000 per year.””It was the Whig Congressman Joseph Chandler that introduced Dyott to Stephen Simpson, a man with a great talent who could write the business plan, the pamphlets and memorials to convince the state legislature to allow Dyott a bank charter. Stephen Simpson approached him about establishing the bank near Dyottville. This made practical business sense, as Dyott explained, in order “to get rid of paying shaving interest to Captain Man.

Stephen Simpson had the combination of banking savvy,political skill, and the capability for rhetorical flourish that Dyott needed. Simpson had been a clerk at Stephen Girard’s bank in the early 1820s. When Girard denied Simpson a promised promotion to the position of cashier, Simpson left the Girard bank and subsequently wrote an especially unflattering biography of the man. Simpson next move was to ally himself with the new Workingmen’s Party, which supported him as a congressional candidate in 1830. He proved himself not only an able bank clerk and populist politician but also a man with a flare for popular rhetoric, which was on display in his Working Man’s Manual and other popular and journalistic writing he did in the 1830s.

His support from the Workingmen’s Party had dissipated by 1832, however, because of his public backing for the Bank of the United States. Simpson was on his way to Washington to take a promised post in Andrew Jackson's administration when Dyott told him about the prospect of writing pamphlets and publishing a new newspaper in order to sway public and political opinion in favor of a bank charter for the Doctor. Simpson agreed to write several pamphlets on Dyottville and publish the new Democratic Herald for the handsome sum of $3,000 per year.

When the Pennsylvania legislature refused to grant Dyott a charter, Simpson aided him in establishing the private “Manual Labor Bank and Six Percent Saving Fund,” a name he likely copied from Rafinesque’s savings institution, next to his patent medicine shop on Second Street in Philadelphia. Dyott’s bank advertised that it was safest of all the savings institutions in the area because it was backed by the $500,000 in real and personal estate of the proprietor himself.

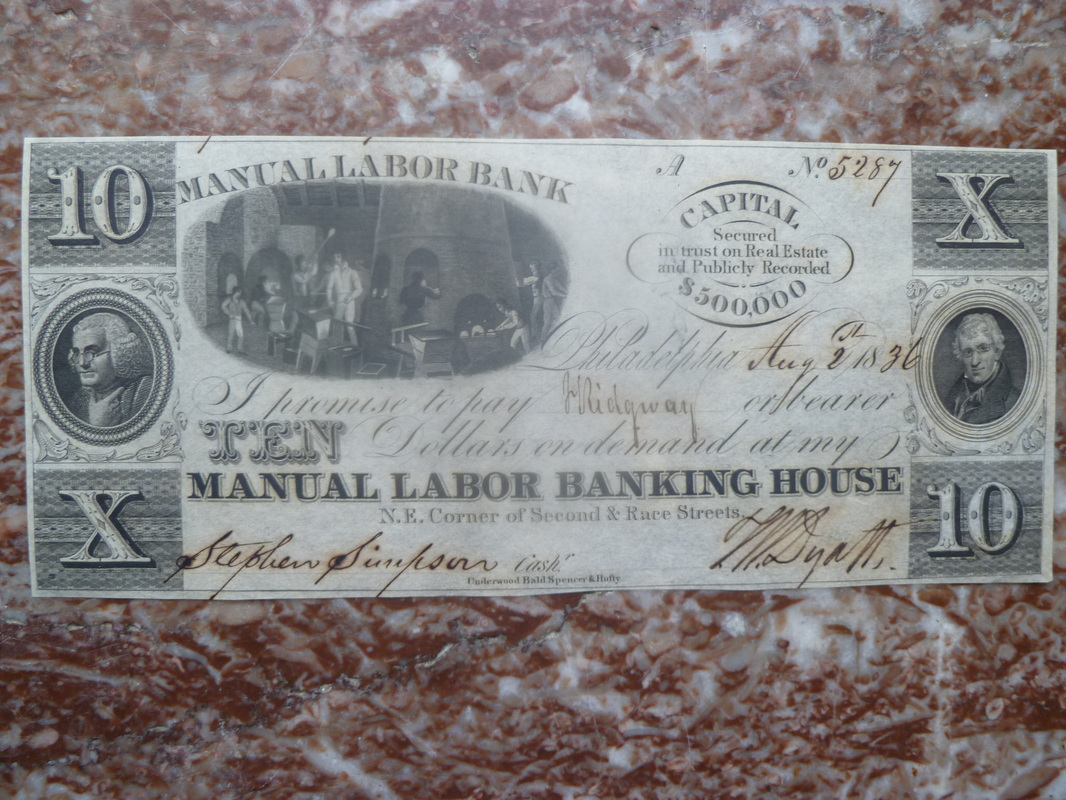

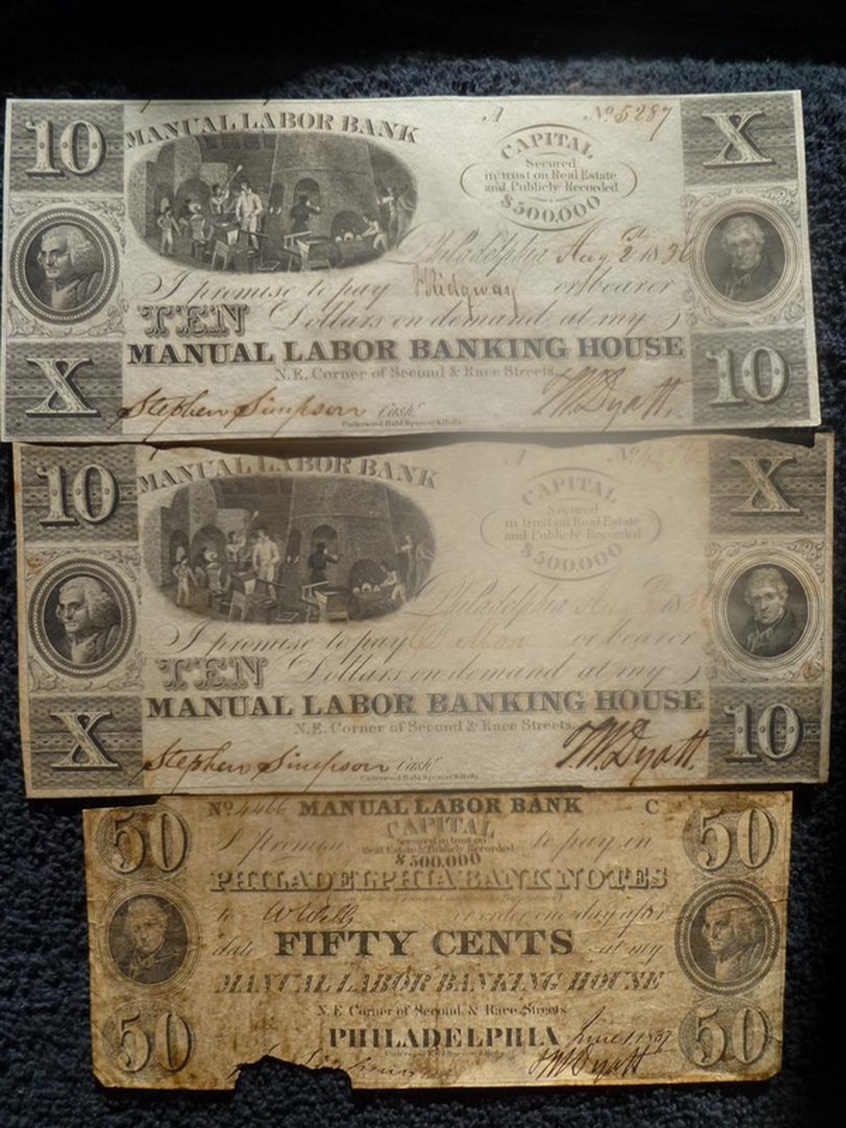

Dyott’s savings institution went into business in February 1836, accepting deposits at 6 per cent and issuing a small amount in bank notes. The funds were used to start paying down his debt to Ridgeway and Man, to finance his current operations, and to make new acquisitions. He soon bought additional property in the vicinity of the patent medicine shop and acquired the stock of Edwards & Veree, a grocer and dry good store, with the intention of expanding his retailing operation . In addition to writing circulars, articles, and other promotional pieces for the new saving fund that promised working depositors the interest they deserved, Simpson served as the institution’s cashier the position he had been denied by Girard. Below is a 10 Dollar Note issued by Dyott and Simpson. It has been made out to J Ridgeway.

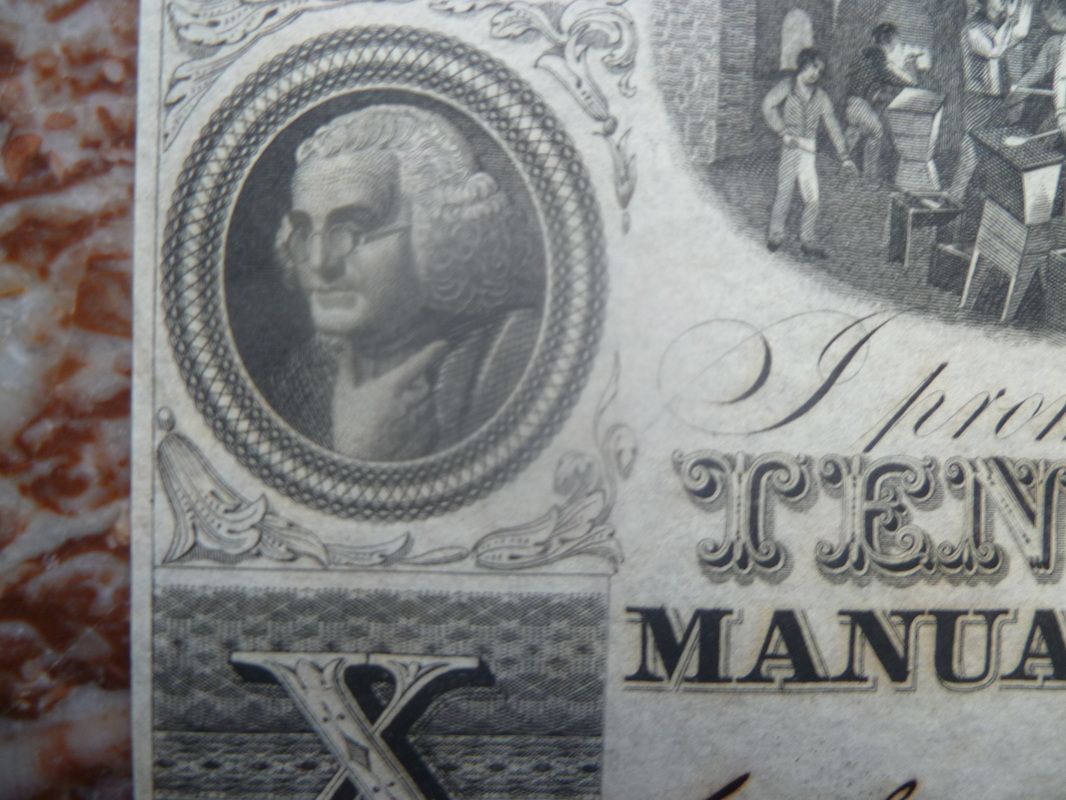

The Bust of Benjamin Franklin in close

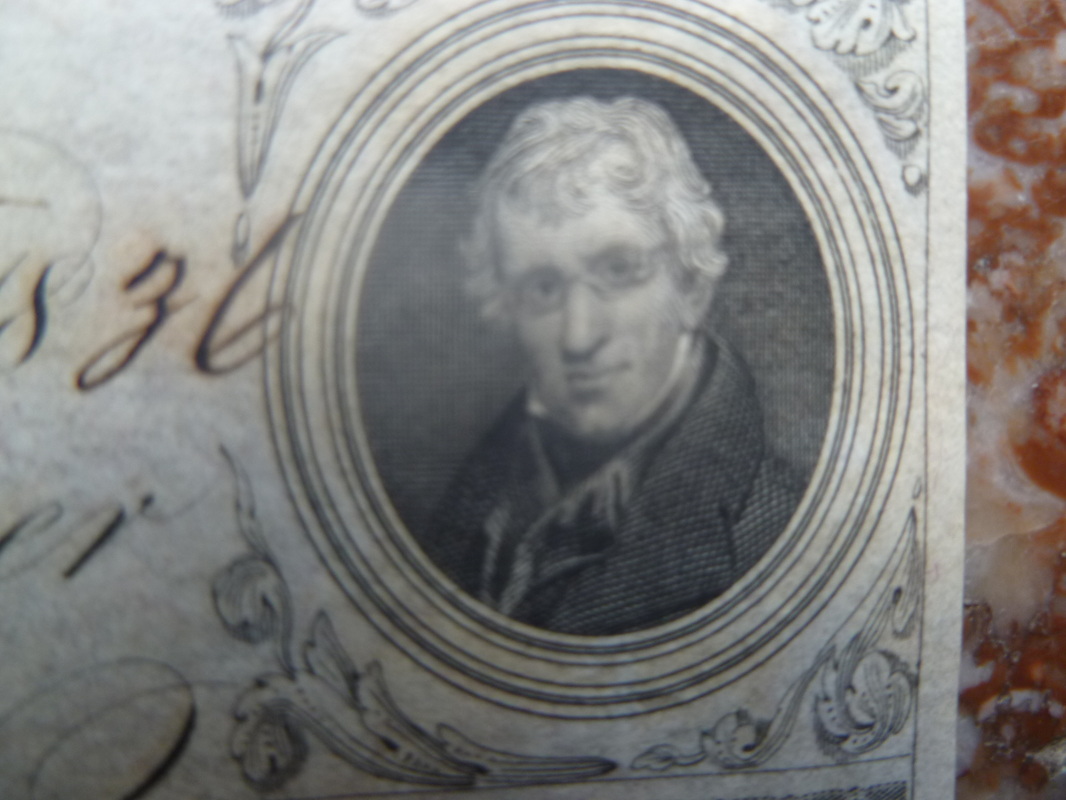

T W Dyotts Portrait in close

The Panic of 1837

The Manual Labor Bank and Saving Fund took its place aside the host of new savings

institutions and loan companies promising higher interest, new services, and innovative features on the premise of serving working-class savers. At least twelve of these were incorporated by the state. Legislative reports estimated that another fifteen or so unincorporated private savings institutions were in existence. Capitalizing on the precedent set by early savings banks, the new institutions that were established in the 1820s and 1830s sought to turn working-class savers into an inexpensive source of funds. Banking and finance , in turn, were rapid transformed into popular business, accessible to all. As one account put it, “Persons who but a few years since had not dared to think of a bank, but as a engine of aristocratic power beheld almost with wonder their names inscribed in bank books as stockholders and depositors. ‘OUR BANK’ was in every mouth.”

By the eve of the Panic of 1837, saving and investing had become a mass market industry. The Panic began in the early Spring of 1837. While historians continue to debate whether domestic or international events triggered the crisis after years of inflation, it is clear that by early 1837 there was a significant contraction in the money supply and an increase in the public’s preference for specie.Depositors in Philadelphia were lined up at their savings institutions as early as February and by April were draining their accounts at near record levels. The movement of specie out of the banks of the Northeast sent interest rates spiraling upwards, and gold and silver coin trading at a significant premium.

Depositors and note holders clamored for their money in coin, destabilizing the savings institutions and loan companies that had only recently been established. Though few records survive from the scores of savings institutions that failed, the archives of the Philadelphia Saving Fund Society showed that the one savings institution that did make it through the crisis – offers some insight into the havoc that the Panic and subsequent depression created on the balance sheets of Philadelphia’s savings institutions. PSFS had experienced significant depositor runs in 1829 and 1834. What was different about the Panic of 1837 was the severity of the runs and, even more important, the prolonged loss of public confidence that followed. The impact was actually felt through a series of runs over five years that were intimately linked together by the fact that public confidence was never restored in between them.

Between January 1837 and January 1843, PSFS lost nearly a third of its depositors and over half of its deposits. According to the PSFS board of Directors, no other financial crisis in the antebellum era compared to the Panic of 1837 in its severity and duration. Not even the Great Depression of the 1930s would impact on the savings bank as the panic of 1837. The impact of the Panic on local savings institutions can only be understood by taking a number of factors into account. The heavy drainage from our deposits must unquestionably be referred to the violent oscillations in our banking system, during the 1830s, and its effects upon our depositors in common with the rest of the community,” explained PSFS’s president to the Board. “It was, moreover, during the same period of excessive expansion and contraction of the currency, that various Savings Institutions successfully rose and sunk in Philadelphia and its suburbs; and by their fall always alarming the fears of our depositors, also aggravated the drainage of our deposits.”

The Manual Labor Banks Failure

Dr. Dyott’s Manual Labor Bank and Six Percent Savings Fund provides a worst case example of the pressures to which these savings institutions finally succumbed. The Manual Labor Bank and Saving Fund had been in operation for just a little over a year when depositors began to demand their money back in specie and high quality banknotes. With circumstances similar to those at PSFS, the financial pressure began in February and was relentless through the Spring. Unlike PSFS, Dyott had no easy way to convert his assets into cash since he had invested the bank’s deposits directly into his various business, buying out the stock of a dry goods merchant named Edwards & Verree, purchasing new properties for his growing retail business and using the funds to finance working capital. He used the deposits of his patrons for personal gain and it came back to bite him in a large way.

Under pressure from depositors, Dyott was once again forced to borrow cash from the

elite merchants on which he had long depended. Jacob Ridgway floated Dyott an emergency loan at a rate of approximately 30 percent per annum and agreed to further lending to the total amount of $50,000 for the coming year. As security,Dyott gave Ridgway a bond on his glassware and other goods, the same property that was “securing” the bank depositors against losses. Dyott used the transaction with Ridgway not only to pay the panicked depositors but also to advertise the personal bond he had issued Ridgway, implying that the highly reputable and wealthy merchant supported the bank showing to the public Dyott's integrity in his savings bank. “The assignment of that bond to Mr. Ridgway, no doubt, contributed greatly to suspend the run upon the Bank, Stephen Simpson later explained. “In May 1837, notices to reclaim deposites from $30 to $50,000 were in the drawer, but after Mr. Ridgeway became Trustee, not $1000 was taken up.”

Over the course of the summer months, Dyott sold off some of the stock of his other retail businesses to his sons and nephew. In July he sold his glassware and drug business to J.B.and C.W. Dyott for $150,000, which was primarily paid for in worthless Manual Labor Notes. He transferred the grocery and dry goods business to his other son, Thomas, Jr. Dyott stated that he did so in order to raise money, to concentrate on the banking business, and to help his sons get set up in business.

Since the Manual Labor Bank and Saving Fund was a private bank secured on Dyott’s personal estate, however, these transfer s potentially weakened the recourse available to depositors in case of the banks failure. In October of 1837, Dyott received early word that rumors had begun to spead through the community about the weakened condition of the Manual Labor Bank and that there was going to be a likely depositor run on the bank. Dyott then used an age old technique that had been employed by other banks, Dyott hired a number of people, friendly to his cause "mostly loyal workers" from his Glass Factory, to arrive at the bank with large packets of money to change or deposit. This quelled the atmosphere momentarily but soon on the horizon was the inevitable and epic failure of all of his business holdings.

Dyott's Empire begins to unravel

John Congden , a resident near the Glass Works had explained to the court during the future trial that Dyott had hired him “to take part in the run upon the Bank. He gave me a bundle of notes, and told me that the depositors who had come to tghe bank that day would see this and would be fooled into believing that the Bank was still very solvent. This act would hopefully restore the confidence in the Bank. In very damning testimony to the court he also stated this transaction was conceived to take up as much time as possible to keep the counter position tied up as long as possible. Again he explained to the court he had presented the first parcel of notes, according to the”instructions. The teller for his part purposely miscounted them three times. As the bank closed for that particular day, Stephen Simpson supposedly, noted to Dyott that he had saved many thousands of his dollars by applying this simple age old technique. It was reported that Dyott spun his hat like a top at his success in avoiding failure that day.

Dyott had avoided only momentarily, the imminent financial ruin that was set to unfold .In the days following the October 1837 run, Dyott needed to change his strategy for dealing with the cash demands of his depositors. Increasingly he was unable to pay depositors in large quantities of high quality bank notes and other cash, instead he instituted a policy of paying them only small amounts – typically less that $5. Their larger withdrawals were met by paying out “Manual Labor notes”that could be redeemed for goods at one of the Dyott stores. Depositors could redeem the notes for drugs or glassware at J.B and C.W. Dyott’s outlet or Thomas Jr’s dry goods and grocery store, both of which were conveniently adjacent to the bank. Dr. Dyott also kept a stock of various goods at his counting house above the store.

To acquire the goods that he himself did not manufacture (such as dry goods and groceries), Dyott used the Manual Labor Bank to issue “post notes” to his suppliers. Post notes essentially IOU certificates redeemable at a future date to the bearer and could circulate. Dyott’s post note issue was at first modest, totally only about $12,000 at the end of 1837. But in the following year he used them to acquire more goods and to pay for services and labor he received. By mid 1838, he had issued $100,000 worth of post notes. Most of the goods purchased with the post notes were in turn placed in the stores of his sons for

depositors to buy.

As the volume of Dyott’s obligations to post note holders increased, some began to question his ability to pay them off in the future, especially given his obligations to depositors as well as to his two largest private lenders, Jacob Ridgway and Daniel Man. During the summer of 1838, the value of the post notes on the open market had dipped to 55 per cent of their face value. Depositors, including his own Dyottville Glass Works employees, began demanding, that he sell off all of his assets to pay off the various creditors. Dyott increasingly began to make more and more desperate moves to salvage his business empire. He very quietly turned over the operation of Dyottville to his brother Michael, and began to sell off his personal assets to raise needed funds. He sold his personal home furniture to his sister-in-law, Julia, for $1,000. Rumors also had begun to circulate that under Dyotts orders large quantities of goods were quietly being removed from the stores and the Glass Works.

The final events that set in motion the Manual Labor Bank's fall into bankruptcy took place in the August of 1838. The Pennsylvania governor announced that he would mandate that financial institutions resume payments in specie, which many of the weaker institutions, including Dyott’s, had in limited supply. What was more telling for the Manual Labor Bank, was that Jacob Ridgway insisted a month later in September that he would re-assign Dyott’s bond. He no longer wanted his good name associated with that of the Manual Labor Bank. This developement led to a complete collapse in the confidence of the bank and by the Fall Dyott’s post notes had a negligible value in the financial market. One month later In October of the year 1838 he announced his intention to file for insolvency.

The Trial of 1839

Dyott’s criminal trial for “fraudulent insolvency” took place during the Spring and the Summer of 1839. What was more unfortunate for him was the economy was sinking back into depression. The key witness for the prosecution was Stephen Simpson who, along with many of Dyott’s other former employees, testified that the Doctor had systematically transferred his assets to his relatives to shelter them from the claims of depositors and other creditors.

Simpson,who had remained steadfastly loyal to Dyott and helped him as much as he could until the bankruptcy, emphatically stated that as early as the summer of 1837 Dyott’s plan was to “render useless the means by which his depositors could obtain legal redress, if they wanted it.” He also poited out to the prosecution that J. Ridgway was also deeply involved in the conspiracy, going as far as to suggesting “Ridgeway was his banker and that it was the prominent merchant who had suggested that Dyott conceal his assets.

Dyott retorted that he had rebuffed Simpson’s attempt to extort the Manual Labor Bank just before it failed and was now testifying in revenge. The main defense argument that was put forward by Dyott’s attorney, seems to have been that Dyott was not conspiring to cheat his depositors, but that he was simply quite naive at banking . “Had the Doctor the simplicity of a child?,” Stated Dyott’s defense attorney to a former clerk, to the amusement of the entire courtroom. “His manners and habits were very plain,” the friendly witness confirmed. “The Doctor knew nothing of book-keeping; nor was he in the habit of examining them.”

The trial left many Philadelphia residents with two interpretations malfeasance or mismanagement for understanding the total failure of Dyott’s savings fund and all the other savings institutions country wide that were in the same predicament. A large percentage were convinced of a conspiracy, and could point to many of Dyott's poor choices as well as the quiet transfer of assets to relatives, his underhanded tactics during the bank runs , the improper use of the names of prominent Philadelphian citizens to imply their support for the bank. Even those less inclined to conjure up the charges and accusations of widespread conspiracy, the wholesale collapse of the savings institutions had highlighted their inherent vulnerability to mismanagement. What was quite apparent though was the complete financial devastation caused by their failure during economic downturns when working depositors needed them most.

Rather than alleviating the distress to the public and reducing the risks of the market economy, these new savings banks had managed to set up their organizations in ways that hastened the spiral down turn felt during the depression. These Banks Promised high returns to the stockholders and depositors. In Dyott's case he delibertly invested their funds in liquid and questionable assets. The managers of these newer savings institutions stood little chance of surviving the Panic and depression and in fact only made matters worse for the good of the community as they failed. Their record early in the depression was far more abysmal than that of the city’s well run commercial banks. In the end however these larger institutions proved to be just as vulnerable. The largest banking institution in the city the Philadelphia Loan Company experienced severe runs and had suspended it operations also by 1839. A similar fate was in store for the Philadelphia Savings Institution because it was also out of business by 1839.

Perhaps in reaction to the Panics and hard times, the board of the Six Percent Savings Fund forced Constantine Rafinesque to resign from the organization even though he was the inventor, founder, and supposedly “it's permanent” director. It appears to have also gone under in the late 1830s. Rafinesque died penniless in 1840. The mercantile community was stunned when Jacob Ridgway was being tried for conspiring with Thomas Dyott to defraud the depositors of the Manual Labor Bank. He managed to keep his good name, and was acquitted on of all the charges. Dr. Dyott also continued to insist he was innocent but convincing a jury of his peers was another matter for he was sentenced to three years imprisonment at the Eastern State Penitentiary. He was 68 at the time of his imprisonment.

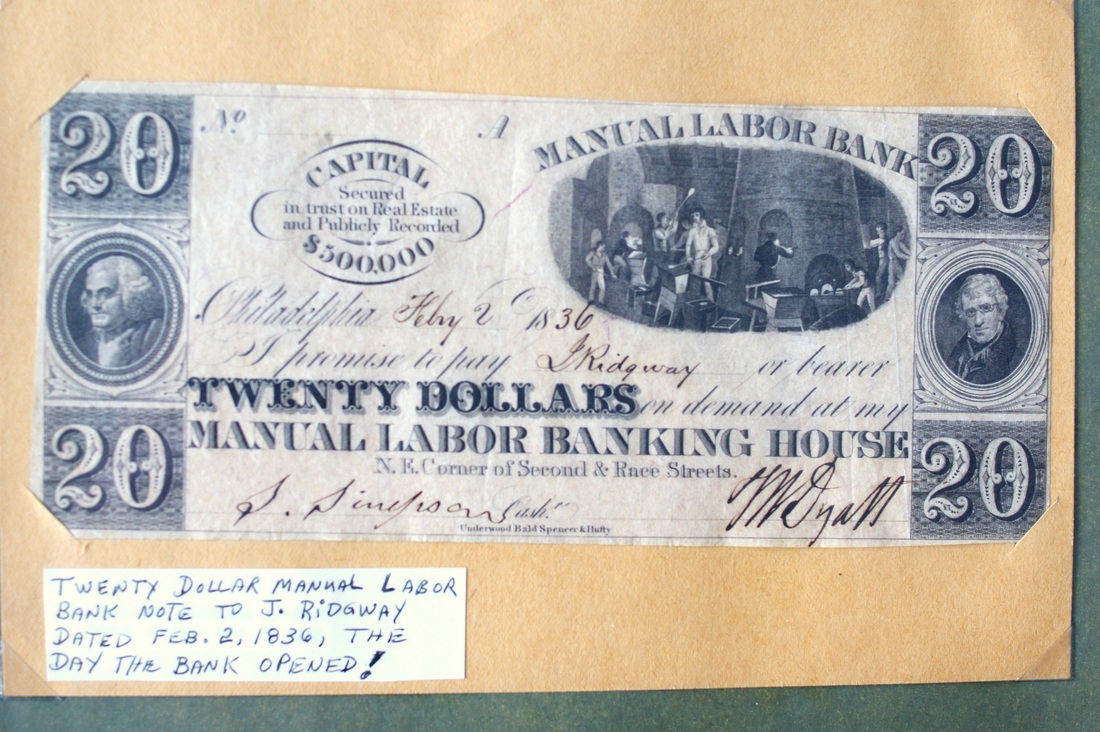

A rare 20 Dollar note dated the day the Manual Bank first opened in Philadelphia.

Below are three notes from the Stephen Atkinson Collection. Two 10 dollar notes and a fifty cent note.

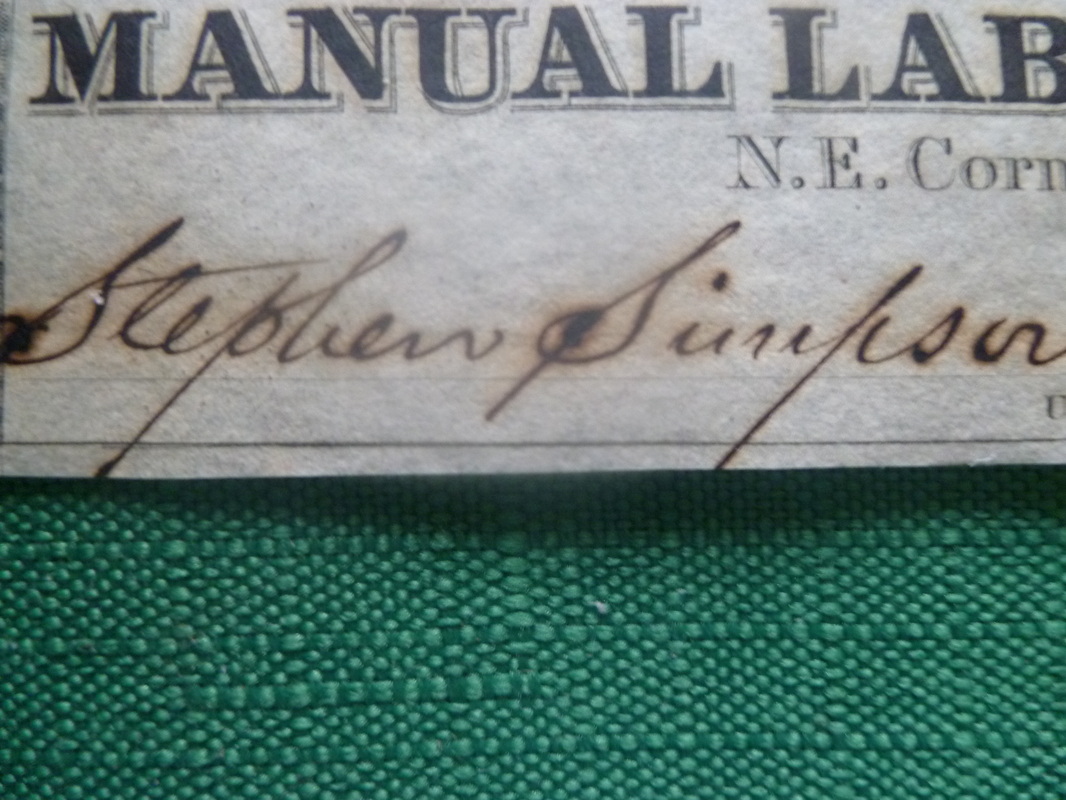

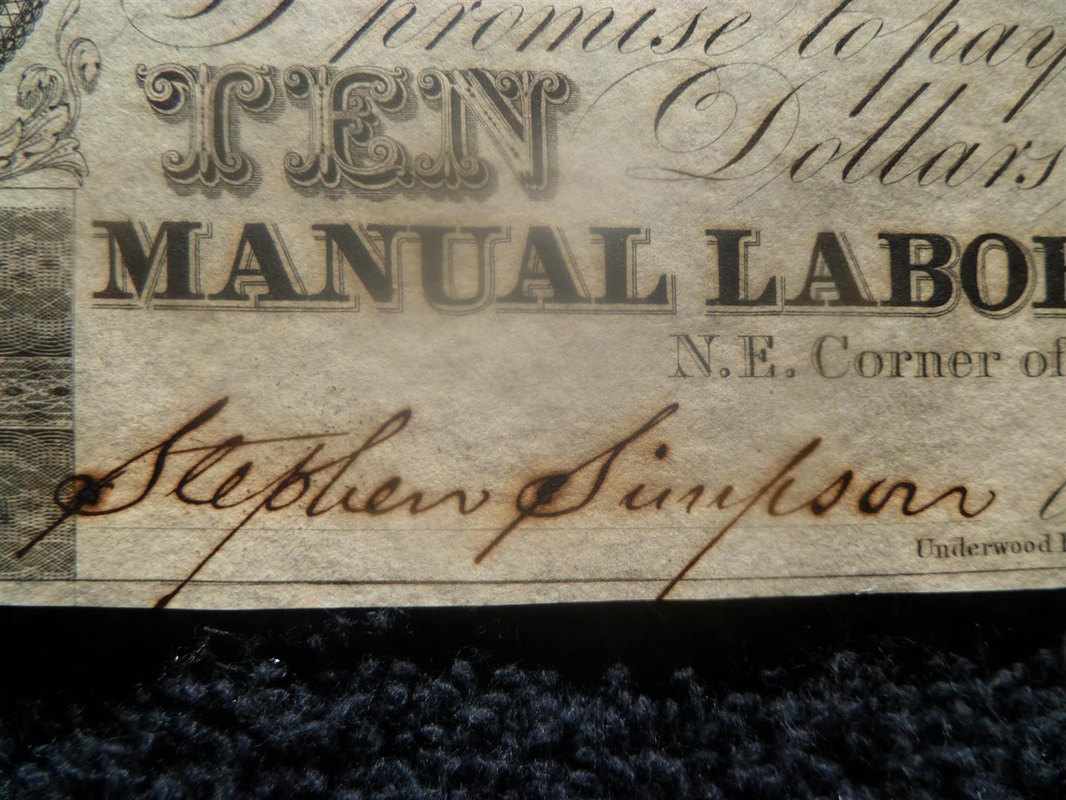

Stephen Simpson's signature below.

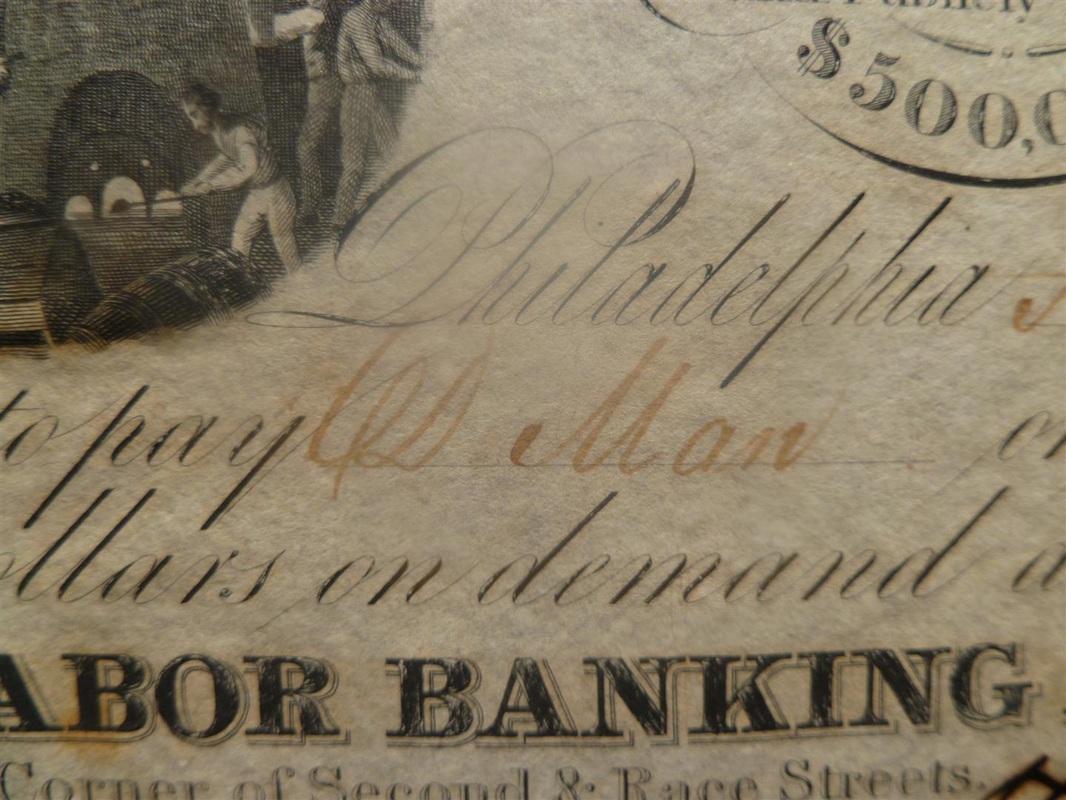

Below,Captain Daniel Man as the bearer of the note.

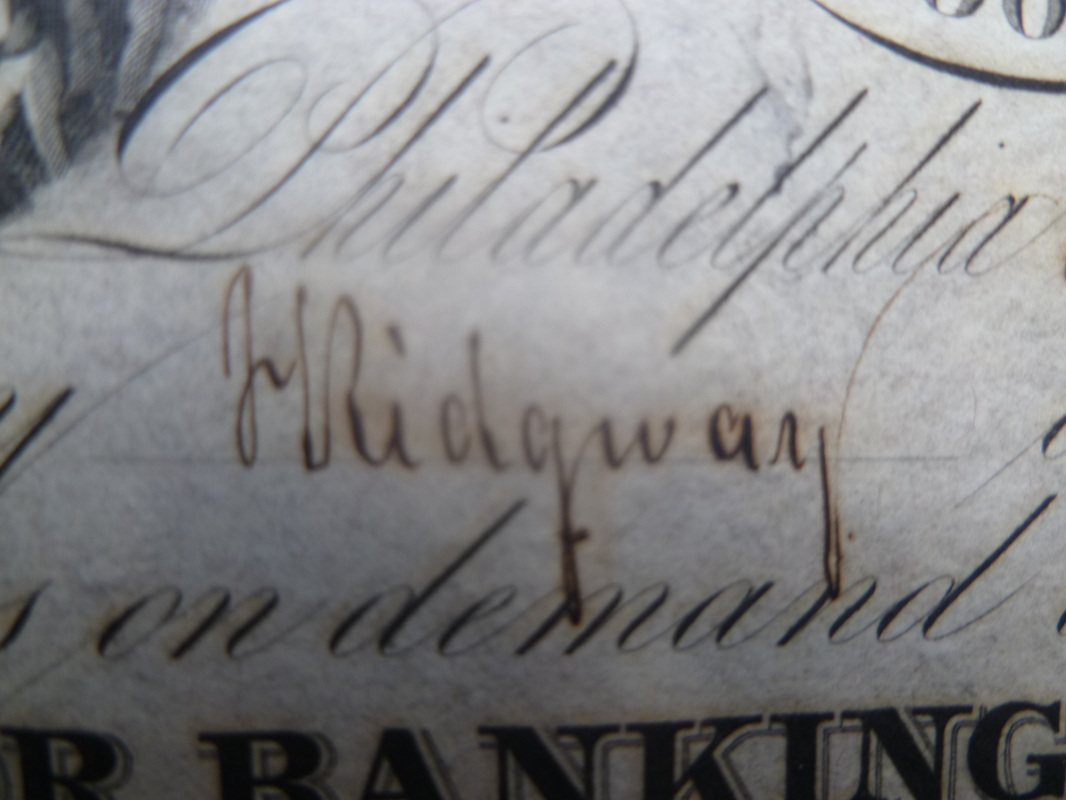

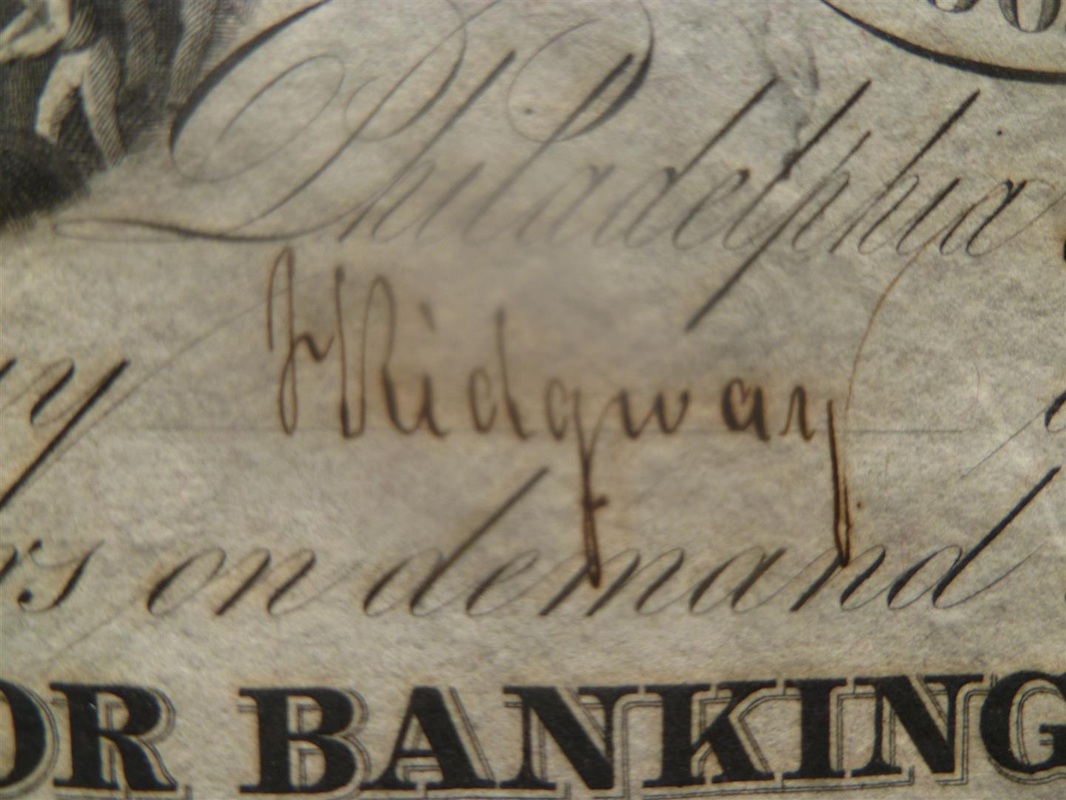

Below the name J Ridgway the Gentleman with the most funds.

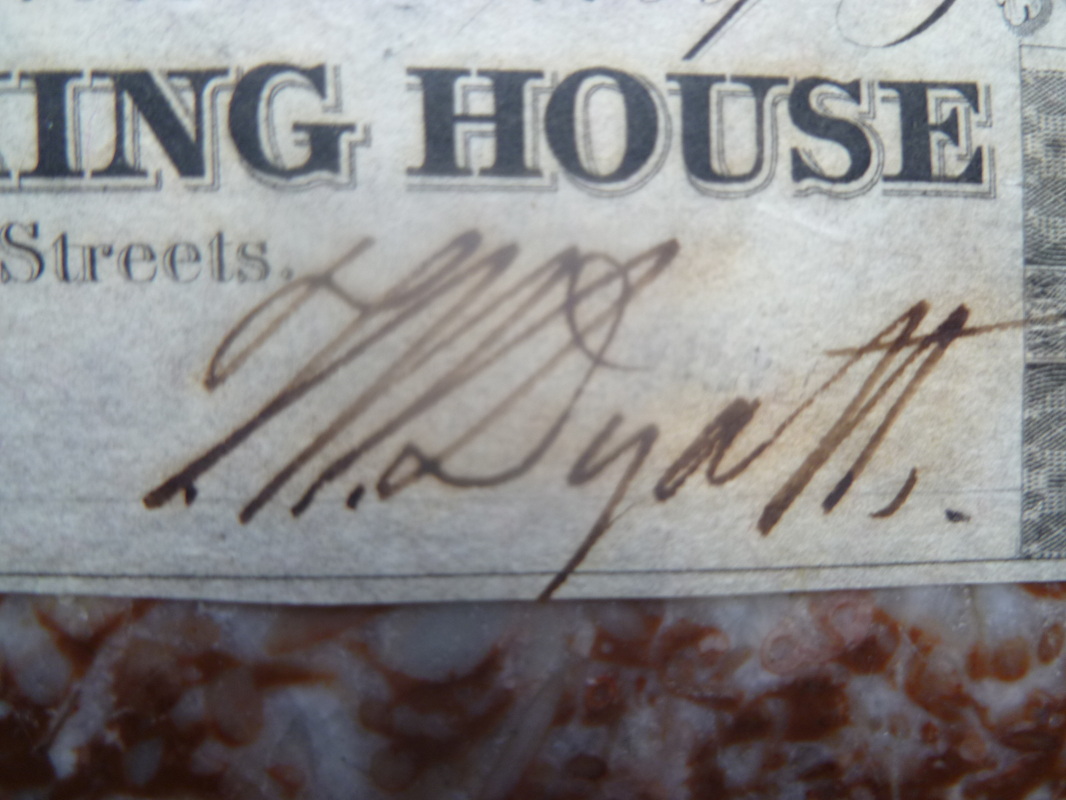

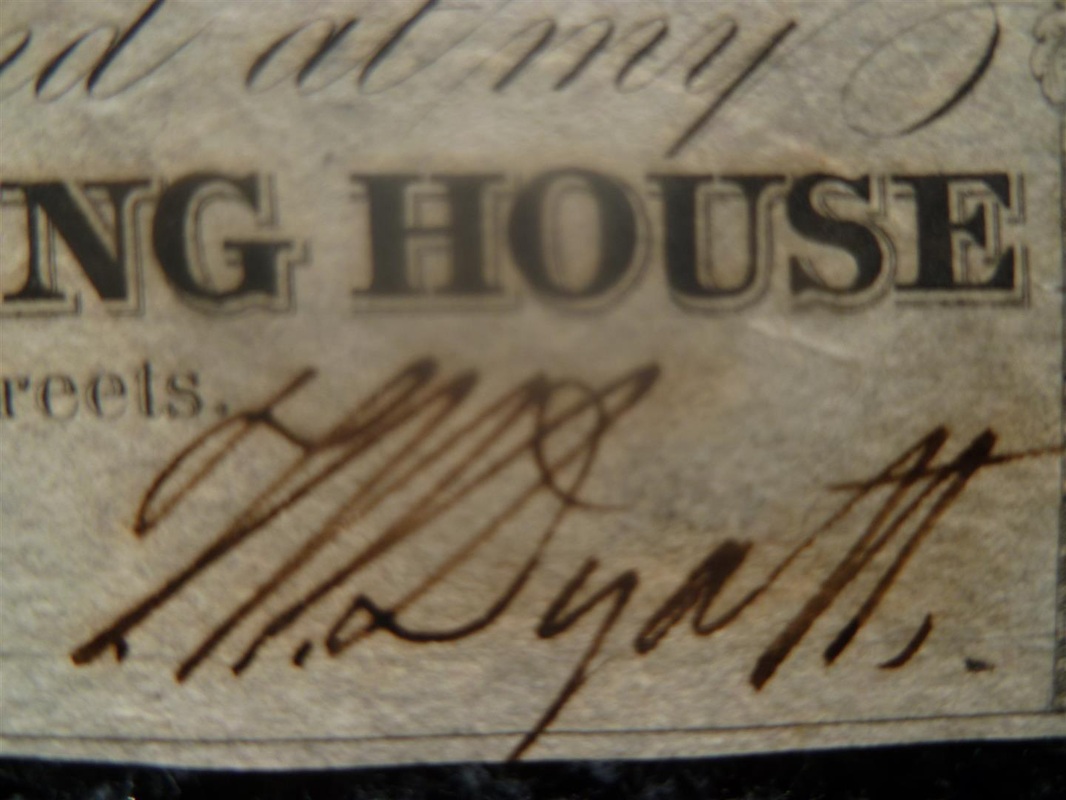

The very famous T W Dyott signature on all of the notes.

The bearer of the 50 Cent note was William Wells a neighbor of Dyott